Step Data Insights #3 (WK 27)

Liquid Staking

This article is not financial advice and is for education purposes only. Always do your own research before investing or trading cryptocurrencies.

Introduction

Welcome to volume three of the Step Finance Newsletter. In this volume, we will conduct analysis on the recent stETH troubles, whether it will potentially collapse, while drawing comparisons to mSOL. In order to proceed with analysis, first we must provide a background to stETH.

Background

Cryptocurrency staking dramatically increased in popularity from 2019 to 2021. This can be demonstrated with the major shift of consensus algorithms from the top 10 cryptocurrencies (by market capitalization) between 2019 to 2021.

During these years, we saw the emergence of cryptocurrencies which utilise PoS mechanisms such as AVAX, SOL, LUNA, and ATOM; all of these cryptocurrencies exploded in popularity, and subsequently price. However, there are two primary criticisms of these emerging PoS cryptocurrencies.

Firstly is their associated lock up periods, an example being Terra (LUNA) which had an in-built lockup period of 21 days, (this caused significant pain for many in the recent crash). Secondly, is the lack of utilisation of value locked. With billions of USD locked up doing very little, accompanied with the emergence of DeFi; we subsequently saw a new innovation called liquidity staking, in the form of Lido Finance.

On Lido Finance, users stake their PoS based cryptocurrencies. They subsequently receive an `st` (staked) version of their cryptocurrency e.g. stETH. With this stETH, users can utilise their staked cryptocurrency of choice through DeFi protocols, while securing the relevant chain / network. This solves the issue of a lack of value utilisation. Additionally, users can sell their `st` cryptocurrency whenever they wish to do so, solving the issue of lockup periods.

Overview

At time of writing, Lido Finance offers liquid staking for five cryptocurrencies. These cryptocurrencies are:

ETH (stETH)

SOL (stSOL)

KSM (stKSM)

MATIC (stMATIC)

DOT (stDOT)

With Lido Finance Dominating ETH liquid staking, it does not have a similar strong hold on SOL. Currently mSOL is 223% larger than stSOL with mSOL holding a value of $253m USD.

All of the above individually have x>$1m USD staked by Lido Finance, although the largest (by total value staked (USD)) is stETH, amounting to 98.2% of total value staked. Overall there are 135k unique stakers currently utilising Lido Finance.

The popularity of stETH has risen exceptionally fast, with the total ETH value topping 7.08m ETH in May 2022, with an ATH staked value of $20.83bn USD.

However, in recent months we have seen significant stETH uncertainty creep in. This is due to the regular negative depegging of stETH to ETH since early May 2022.

Negative depeging has not been a trend across the liquid staking industry, rather it has been the opposite. This can be effectively displayed with both stSOL and mSOL (both of which can be redeemed for SOL). Both liquid staking solutions are trading closely to the SOL peg, and have often been trading at a positive depeg above the SOL market price, benefiting bullish market participants.

Why is This Occurring?

The primary identified reason for stETH trading below the market price is due to the Lido Finance stETH peg mechanics. If the price of stETH falls below the market price of ETH, you can purchase stETH and redeem it for an increased amount of ETH, allowing arbitrage traders to generate potential profit. However, this mechanism is currently not in place due to Ethereum2.0 remaining inactive. Instead, Lido Finance are reliant on incentivised liquidity mining with the ETH / stETH pair on various DeFi applications e.g. Curve Finance.

The issue with this, is that if there is a lack of liquidity across these protocols, then stETH is more susceptible to a depeg of its 1:1 ETH price due to stETH being currently non redeemable. Due to global bearish market conditions, overall liquidity across cryptocurrency market DEX’s has dropped significantly, which has increased stETH’s susceptibility to a depeg.

Overall, we have seen TVL in DEX’s fall by $19bn USD (01/04/2022) to $6.66bn USD (05/07/2022) with an overall TVL reduction of 65%. From DEX’s analysed, we can see that CRV have been the primary sufferers with a TVL decrease of 83%.

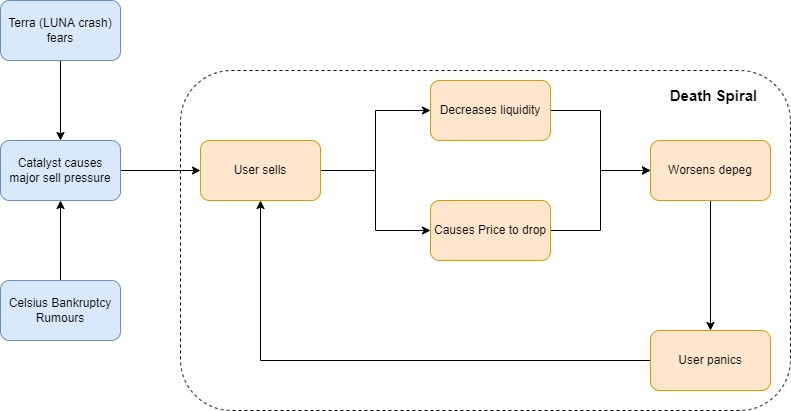

During this period the total DeFi market capitalization to TVL ratio has fallen from 8.78 to 6.45. This negative change of 2.33 represents a decline in strength of the DeFi market, and has caused numerous projects in the DeFi space to suffer. One example project which the liquidity crisis / bear market has caused massive damage is Fabric (synthetics based platform on Solana) who recently had to shut shop. Along with this liquidity crisis, stETH has been subjected to two major catalysts, with those factors being the Terra (LUNA) collapse, and Celsius bankruptcy rumours. This has caused stETH to enter a slight death spiral, as shown below.

Will This End Like LUNA? Is my stSOL / mSOL Safe?

Unlike LUNA & UST, there are significant differences with stETH and stSOL. What we are witnessing with stETH is a secondary free market for ETH due to the current failings of the incentivised stETH / ETH liquidity pools. In this secondary market for ETH, there are increased fears due to LUNA, and Celsius. Overall, the current conditions for ETH are superior to stETH. When coupled with a lack of liquidity (and Celsius sell pressure) we have subsequently seen stETH forced below its peg, despite stETH being 1:1 redeemable for ETH.

From analysis, it seems extremely unlikely that individuals stSOL, stETH, or mSOL will be unsafe. Furthermore, should an extreme depeg occur, significant opportunities could arise. However, stETH and wstETH is utilised across numerous DeFi protocols (on both Ethereum and Solana) and could trigger an array of unseen issues should a mass depeg occur.

Current SOL State of Play

At time of writing, we can currently see that 75.2% of Solanas circulating supply is being staked, creating a staking ratio of approximately 3:4. With a current market capitalization of $12.7bn USD, we can determine that the value staked sits at $9.57bn USD which equates to 258.6m SOL. Collectively Lido Finance and Marinade have a total of 8.75m SOL staked between them. With Lido Finance and Marinade the two primary players of the Solana liquid staking space, we can derive that only 3.38% of SOL staking is liquid staking. This is a surprisingly low percentage when accounting for the potential benefits of liquid staking. Whether this trend will change remains to be seen. However, this high percentage of locked tokens despite the bearish trend displays community strength and belief from institutions, organisations, and individuals within the Solana ecosystem.

Conclusion

We are currently witnessing an interesting predicament occurring with stETH. Fortunately users' funds are safe, even if stETH significantly loses its peg, it seems majorly unlikely that it would not regain it. The primary underlying issue of this whole debacle is Ethereum 2.0. As shown with the current stSOL situation, even if there is a lack of liquidity, if you can successfully redeem your stSOL for SOL, then arbitrage traders will ensure that the peg is maintained.

Ultimately, if Ethereum 2.0 was on time, and was not three years late, we would be analysing something else this week.

Author: @page_analyst